I came across the Telstra Super Calculator recently and it is quite good. It is now officially my favourite calculator! It can be found here.

If you haven’t used this yet, it is highly recommended as it has a number of features which can help early retirees, and also has a number of unique features.

It has the following features:

- It allows you to Retire at any age (many calculators enforce a minimum limit)

- It allows you to contribute money to Super (as a non-concessional contribution). Unfortunately it does not allow you to contribute more than $180,000 (i.e. no accommodation for the “Bring Forward” rule), and also only allows you to contribute prior to retirement.

- It allows you to see how your plans would fare in various typical Super performance scenarios.

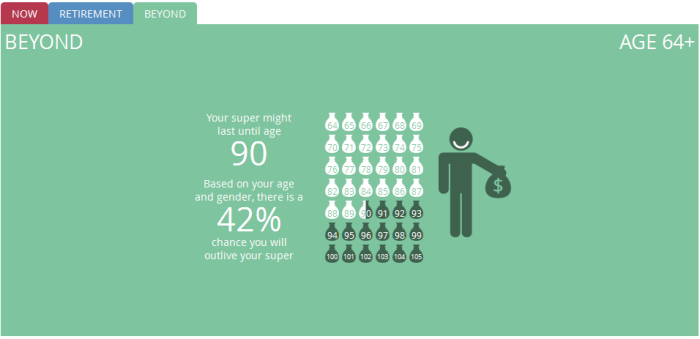

- It includes information on how likely you are to outlive your super.

Unfortunately it doesn’t support many of the features required to properly model early retirement:

- It doesn’t allow you to survive on cash prior to accessing Super. It forces you to start spending your Super at 60 if you are retired earlier that 60.

- It doesn’t allow you to contribute to Super after your are retired.

- It doesn’t support the “Bring Forward” rule when making contributions prior to retirement.

- It doesn’t support different levels of spending as you age.

- It doesn’t support logical mortality-based decisions on reduced spending as you age.

Still, it is a nice calculator. It’s not actually in the interests of these Super companies to support modelling early retirement as they would like to encourage you to work as long as possible (so that you can lodge nice large balances with them!).

I would like to compare this calculator to all the other calculators I have looked at, but unfortunately legislation has changed since then, so it is no longer possible.

I will show here how it can be used in my situation as of beginning of 2016.

Using the Calculator

For my situation, I will once again have to model using starting at 64, because the calculator does not support the Bring Forwards rule and living on cash prior to retirement.

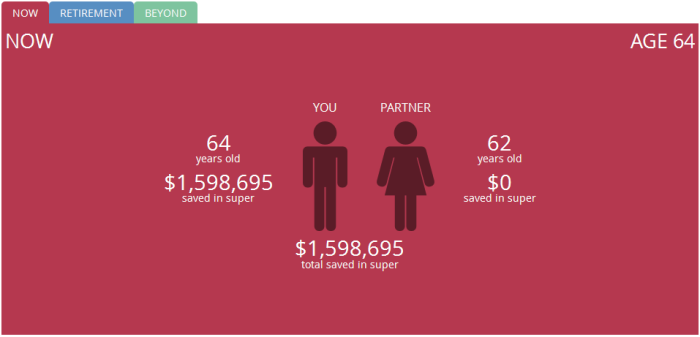

Given the assets at the beginning of 2016 (Cash $708K, Super $615K), the amount of Super I will have at 64 is now calculated to be $1,598,695 in 2016 dollars. Note I have removed the reduction in spending at 70 and 80. If I now use the calculator and set:

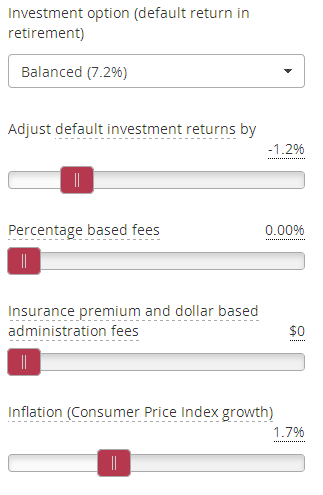

- My retirement age to be 64 and my spouse to 62.

- An investment income of $5,136

- An investment asset of $260K

- Use the Balanced return of 7.2%, adjusted by -1.2% (for a return of 6%)

- Percentage fees to 0%

- Insurance premiums to $0

- Inflation to 1.7% (1.7% because the Telstra calculator uses a wage inflation discount of 1%, and I do not use this)

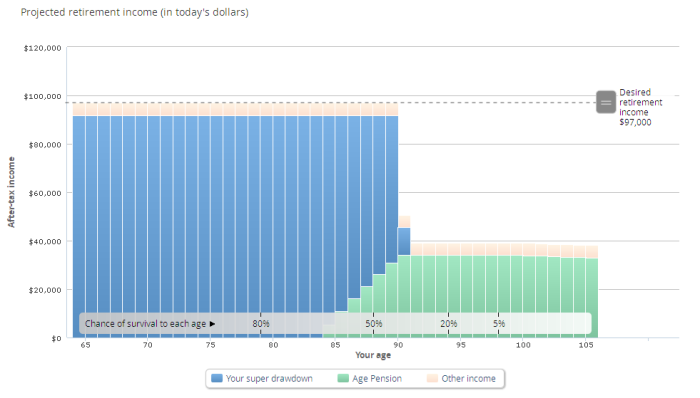

Then the Telstra calculator produces this:

My calculator comes up with $98,500, so this is pretty close. Note that the Pension doesn’t cut-in until 84. This is because of this assumption relating to the calculator:

” In the projection, the Age Pension is indexed with wage inflation, while the asset and income test thresholds are indexed in line with price inflation.”

Because I am effectively discounting the Age pension by the inflation rate rather than wage inflation, this means the Age pension is indexed to inflation and the asset and income test thresholds are discounted by inflation less 1% (Hence the later Pension age, and also the slightly lower overall spend). Or in other words, I can’t exactly map my model to the Telstra assumptions.

There are ten investment performance scenarios that can be tested. Here are the results, showing the age at which funds run out:

The average is 90.4, and standard deviation 4.75. This can be compared with my More on Risk post, which does something similar (except 64,000 scenarios are tested!).

Conclusions

The Telstra calculator is a nice calculator and has some features which can help the early retiree. If you are nearing retirement, I recommend you give it a go.